Intro

Unlock the full potential of your military pension with these expert tips. Discover 5 proven strategies to maximize your military retirement benefits, including pension optimization, tax savings, and investment growth. Learn how to make the most of your military pension and secure a comfortable post-service life.

Serving in the military is a noble and selfless act that requires immense sacrifice and dedication. One of the benefits of serving in the military is the pension that comes with it. A military pension can provide a steady stream of income in retirement, helping to ensure a comfortable and secure financial future. However, many military personnel and veterans are not aware of the ways to maximize their military pension. In this article, we will explore five ways to maximize your military pension.

Understanding Your Military Pension

Before we dive into the ways to maximize your military pension, it's essential to understand how it works. A military pension is a defined benefit plan, which means that the benefit amount is based on a formula that takes into account your years of service and final pay grade. The pension is typically calculated as a percentage of your final pay grade, multiplied by the number of years you served. For example, if you served for 20 years and your final pay grade was $50,000, your pension might be 50% of that amount, or $25,000 per year.

How to Calculate Your Military Pension

To calculate your military pension, you can use the following formula:

- Multiply your years of service by 2.5%

- Multiply the result by your final pay grade

For example, if you served for 20 years and your final pay grade was $50,000, your pension would be:

- 20 years x 2.5% = 50%

- 50% x $50,000 = $25,000 per year

1. Serve for at Least 20 Years

One of the most effective ways to maximize your military pension is to serve for at least 20 years. This is because the pension calculation formula multiplies your years of service by 2.5%. The more years you serve, the higher your pension will be. Serving for 20 years or more also qualifies you for a higher pension percentage, which can significantly increase your benefit amount.

The Benefits of Serving for 20 Years or More

Serving for 20 years or more has several benefits, including:

- Higher pension percentage

- Increased benefit amount

- Eligibility for other military benefits, such as healthcare and education assistance

2. Increase Your Final Pay Grade

Another way to maximize your military pension is to increase your final pay grade. This can be achieved by advancing in rank or receiving promotions. A higher final pay grade will result in a higher pension benefit amount. For example, if you're able to increase your final pay grade from $50,000 to $60,000, your pension benefit amount will increase by $5,000 per year.

How to Increase Your Final Pay Grade

To increase your final pay grade, you can:

- Advance in rank through promotions

- Take on additional responsibilities or leadership roles

- Pursue education and training opportunities to enhance your skills and qualifications

3. Take Advantage of the REDUX Option

The REDUX option is a pension plan that allows military personnel to receive a $30,000 bonus at the 15-year mark in exchange for a reduced pension benefit amount. The REDUX option can be a good choice for those who need a lump sum of money to pay off debt or cover other expenses. However, it's essential to carefully consider the pros and cons before making a decision.

The Pros and Cons of the REDUX Option

The pros of the REDUX option include:

- Receiving a $30,000 bonus at the 15-year mark

- Having a lump sum of money to cover expenses or pay off debt

The cons of the REDUX option include:

- Reduced pension benefit amount

- Potential impact on long-term financial security

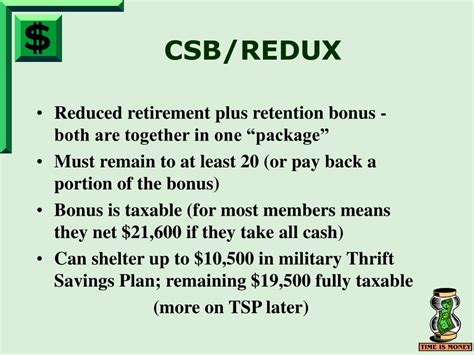

4. Consider the CSB/REDUX Option

The CSB/REDUX option is a pension plan that combines the Career Status Bonus (CSB) with the REDUX option. This plan provides a $30,000 bonus at the 15-year mark, as well as a reduced pension benefit amount. However, the CSB/REDUX option also includes a provision that allows military personnel to opt out of the REDUX option at the 20-year mark and receive a higher pension benefit amount.

The Pros and Cons of the CSB/REDUX Option

The pros of the CSB/REDUX option include:

- Receiving a $30,000 bonus at the 15-year mark

- Having the option to opt out of the REDUX option at the 20-year mark

- Receiving a higher pension benefit amount

The cons of the CSB/REDUX option include:

- Reduced pension benefit amount if the REDUX option is not opted out

- Potential impact on long-term financial security

5. Seek Professional Advice

Finally, it's essential to seek professional advice when it comes to maximizing your military pension. A financial advisor who specializes in military benefits can help you navigate the complex world of military pensions and make informed decisions about your financial future.

How to Find a Financial Advisor

To find a financial advisor who specializes in military benefits, you can:

- Ask for referrals from fellow military personnel or veterans

- Check with professional organizations, such as the Financial Planning Association (FPA)

- Research online and read reviews from other clients

By following these five tips, you can maximize your military pension and ensure a secure financial future. Remember to always seek professional advice and carefully consider your options before making any decisions.

We hope this article has been informative and helpful. If you have any questions or comments, please feel free to share them below.

How is my military pension calculated?

+Your military pension is calculated by multiplying your years of service by 2.5% and then multiplying the result by your final pay grade.

What is the REDUX option?

+The REDUX option is a pension plan that allows military personnel to receive a $30,000 bonus at the 15-year mark in exchange for a reduced pension benefit amount.

How can I maximize my military pension?

+You can maximize your military pension by serving for at least 20 years, increasing your final pay grade, taking advantage of the REDUX option, considering the CSB/REDUX option, and seeking professional advice.